%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

Land contamination poses risks to both health and the environment, often requiring extensive remediation efforts, and the costs associated with remediation can be substantial, particularly for property owners and developers. The UK government often offers various forms of land remediation relief and forms of support to facilitate the clean up and redevelopment of contaminated land and buildings. The land remediation relief tax incentive offers enhanced tax relief to UK companies who incur expenditure in remediating contamination on land or in buildings, or when dealing with derelict buildings.

Land is contaminated for Land Remediation Relief purposes if there is something which could cause harm to living organisms, pollute controlled waters, impact on ecosystems or cause structural damage to buildings, such as asbestos, lead/copper/zinc/heavy metals, sulphurous materials/hydrocarbons, Japanese knotweed, radon and arsenic.

What types of relief are available and the rates of relief available?

The types of relief generally available are as follows and vary between an individuals involvement with the land and the financial status of the company. An owner, occupier or investor can receive up to 150% tax relief whereas a property developer is eligible for 50% relief. A loss making business can receive 16% relief as a cash credit.

The government outlines some conditions that must be met to be eligible to receive land remediation relief. These conditions are listed below:

· The expense would not have been necessary if the land were not contaminated

· There is no grant or subsidy available for this expenditure

· The pollution was neither caused nor exacerbated by any actions or inactions of the claimant

· The expenditure does not qualify for any tax relief under Capital Allowances

· A significant interest in the land is held, either as a freehold or with a lease of at least 7 years.

1. How long do I have to claim?

A claim for land remediation relief can be made in the relevant tax return. For qualifying Revenue expenditure, a company claims land remediation relief when the land or property is sold. For capital expenditure deduction is allowed in the tax computation for the accounting period in which the capital expenditure is incurred. A backdated claim must be made by amending the tax return. The time limit is up to four years after the end of the accounting period for which the claim is made.

2. Who can claim land remediation relief?

Land remediation relief is corporation tax relief. Therefore, the relief is available for expenditure incurred by tax paying limited companies. Land remediation relief is not available for individuals or partnerships.

3. Who can undertake the remediation work?

The remediation work may be undertaken directly by the company or on its behalf.

4. I have received a grant towards the remediation works, can I still claim?

If the land remediation expenditure is greater than the subsidy or grant received, then the balance of expenditure can qualify.

5. How RCK Partners can help with your land remediation relief claim?

RCK are a London-based tax consultancy, specialising in tax-saving services including Land Remediation Relief. With our unique self-regulation approach, each claim we submit to HMRC is reviewed by our independent, in-house compliance and review team. The team has a combined 125 years of experience within property tax and is comprised of architects, surveyors, and property specialists. We will handle the entire process from scoping to submission and beyond on your behalf to minimise the time input required from your side.

Contact our team with your enquiry or to begin the process of claiming land remediation relief.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

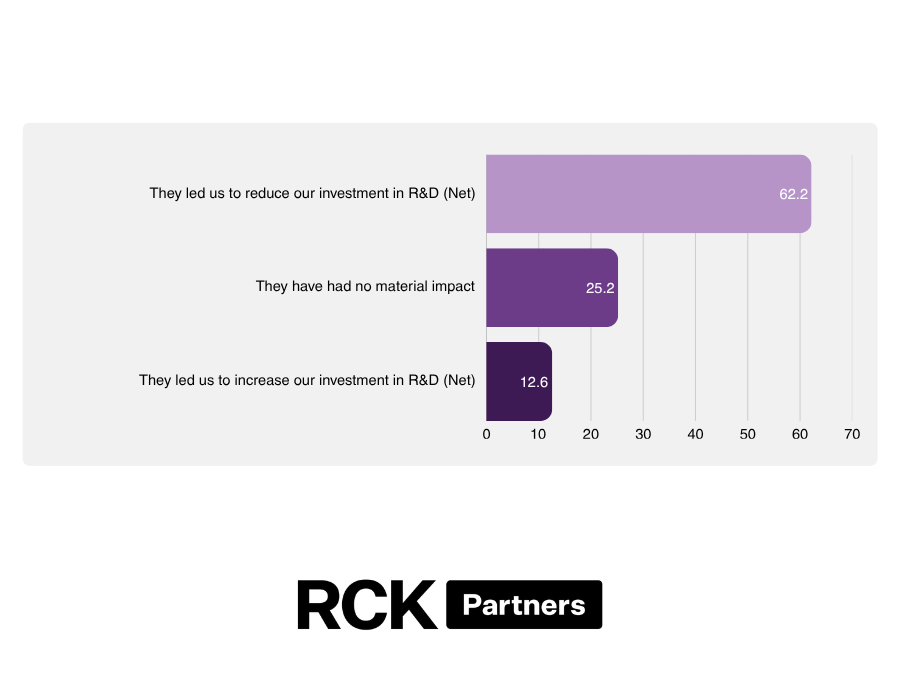

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.